")

Co-living vs flat rentals in Bengaluru: a data-driven comparison (2026)

Data sources: Flat rental data from bengaluru.rent. Co-living property and pricing data sourced from Zolo, Stanza and HelloWorld via Instadwell. Analysis covers 285+ co-living properties and 4,500+ flat listings across Bengaluru as of 2026.

The headline numbers

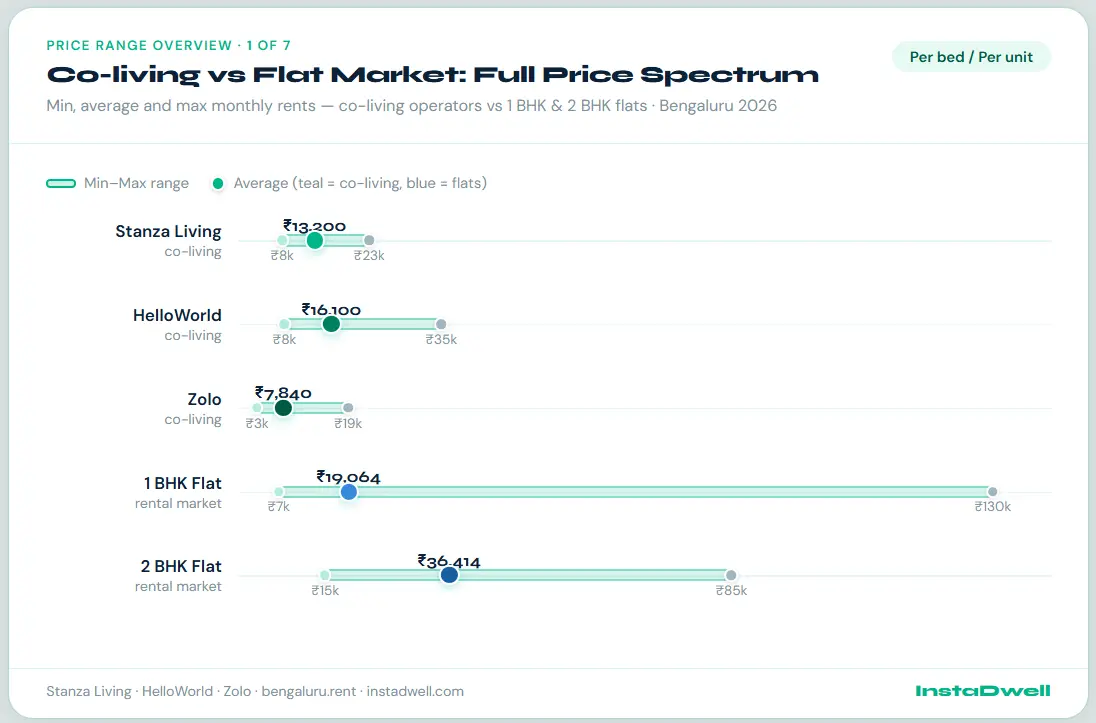

Bengaluru is one of India’s most expensive rental markets. The city-wide flat average sits at roughly Rs 19,064/month for a 1 BHK and Rs 36,414 for a 2 BHK. Co-living beds, by contrast, average around Rs 12,900/month and fall as low as Rs 3,272 at the budget extreme.

But that raw comparison obscures a far more interesting story. Co-living is not a monolith. Across three operators, Stanza Living, HelloWorld, and Zolo, you find three completely different market strategies, price ceilings, geographic footprints, and target customers. And in specific neighbourhoods, those strategies produce some genuinely surprising anomalies.

This report unpacks all of it.

City-wide snapshot

| Metric | Figure |

|---|---|

| Co-living avg rent | Rs 12,900 / bed / month |

| 1 BHK flat avg | Rs 19,064 / month |

| 2 BHK flat avg | Rs 36,414 / month |

| 3 BHK flat avg | Rs 62,591 / month |

| Co-living properties tracked | 285+ across 3 operators |

| Furnished flat premium vs unfurnished | +22% (Rs 21,989 vs Rs 17,982) |

| Gated society premium vs non-gated | +15% (Rs 20,736 vs Rs 18,042) |

City-wide snapshot of rental averages and property premiums

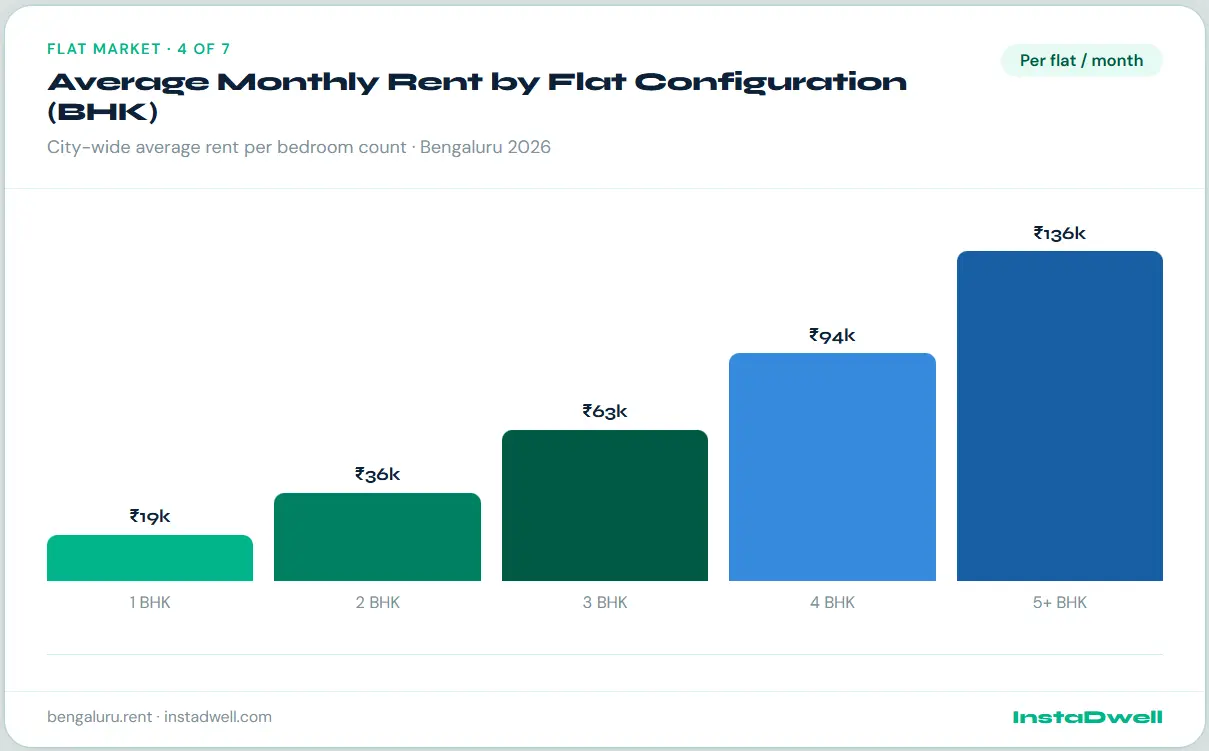

The flat market curve

When looking outside of co-living, upgrading your space in Bengaluru comes with an aggressive premium. The data reveals a steep exponential curve as you add bedrooms to a standard flat:

- 1 BHK: ₹19k / month

- 2 BHK: ₹36k / month (an 89% jump from 1 BHK)

- 3 BHK: ₹63k / month (a 75% jump from 2 BHK)

- 4 BHK: ₹94k / month (a 49% jump from 3 BHK)

- 5+ BHK: ₹136k / month

This aggressive scaling is why splitting larger flats (3 BHKs and above) becomes harder to justify on a per-room basis compared to premium co-living options, keeping the primary flat rental debate heavily focused on the 1 and 2 BHK configurations.

Average Monthly Rent by Flat Configuration (BHK) in Bengaluru (2026)

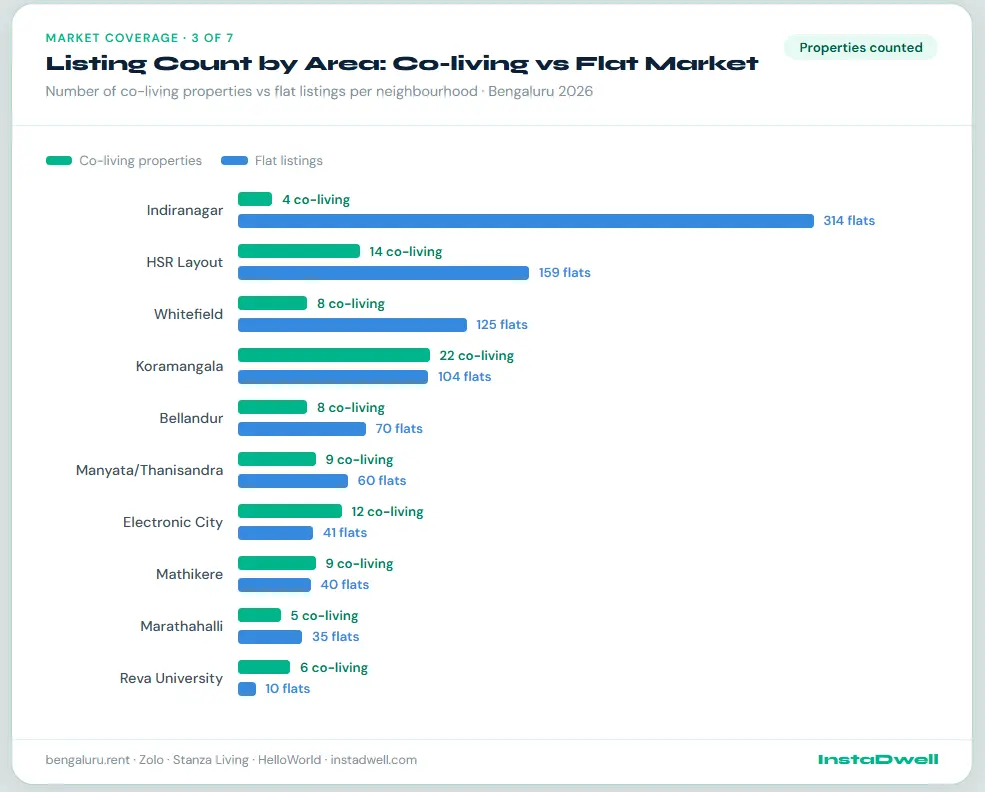

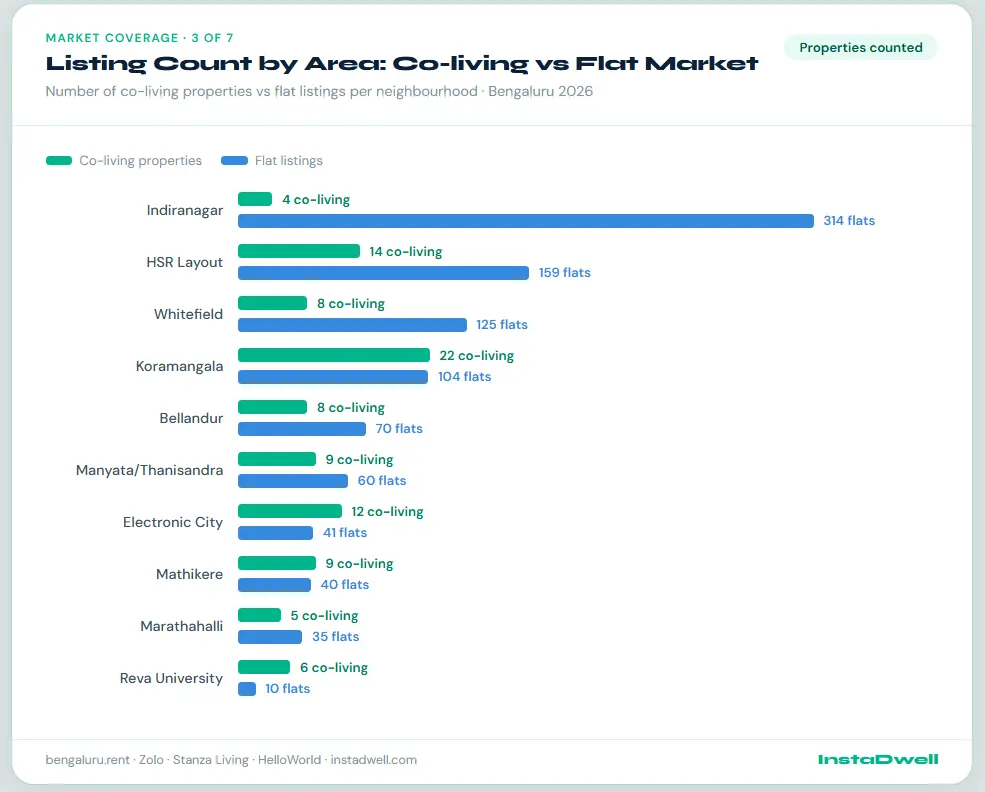

Section 1: Supply density - Where is the inventory?

Before looking at prices, you have to look at availability. The market coverage across Bengaluru’s key neighbourhoods reveals stark differences in how traditional landlords and corporate co-living operators view the city.

| Neighbourhood | Co-living properties | Flat listings | Ratio (Flats per Co-living property) |

|---|---|---|---|

| Indiranagar | 4 | 314 | 78.5 to 1 |

| HSR Layout | 14 | 159 | 11.3 to 1 |

| Whitefield | 8 | 125 | 15.6 to 1 |

| Koramangala | 22 | 104 | 4.7 to 1 |

| Bellandur | 8 | 70 | 8.7 to 1 |

| Manyata/Thanisandra | 9 | 60 | 6.6 to 1 |

| Electronic City | 12 | 41 | 3.4 to 1 |

| Mathikere | 9 | 40 | 4.4 to 1 |

| Marathahalli | 5 | 35 | 7.0 to 1 |

| Reva University | 6 | 10 | 1.6 to 1 |

The Indiranagar void: Indiranagar is heavily dominated by traditional flats (314 listings to just 4 co-living properties). The high real estate costs and entrenched residential nature make it incredibly difficult for density-based co-living operators to acquire properties at a viable margin.

The Koramangala concentration: Koramangala is the undisputed co-living capital of Bengaluru. With 22 properties tracked, it has the highest concentration of branded beds in the city, operating alongside a highly active (104 listings) traditional flat market.

The student/entry-IT corridors: Areas like Electronic City (12 co-living vs 41 flats) and the Reva University belt (6 co-living vs just 10 flats) show how operators intentionally target zones with massive influxes of students and entry-level IT workers where traditional flat supply simply cannot keep up with demand.

Listing Count by Area: Co-living vs Flat Market in Bengaluru (2026)

Section 2: What does a solo professional actually save?

The most common question around co-living is simple: compared to renting a flat, how much cheaper is it? The answer depends heavily on which flat you are comparing against.

All figures below use the city-wide co-living average of Rs 12,900/bed/month. Flat figures are city-wide averages from bengaluru.rent.

| Flat benchmark | Flat avg (Rs) | Co-living (Rs) | Monthly saving (Rs) | % saved |

|---|---|---|---|---|

| 1 BHK city average | 19,064 | 12,900 | 6,164 | -32% |

| 1 BHK gated society | 20,736 | 12,900 | 7,836 | -38% |

| 1 BHK furnished | 21,989 | 12,900 | 9,089 | -41% |

| 1 BHK unfurnished | 17,982 | 12,900 | 5,082 | -28% |

| 2 BHK solo occupancy | 36,414 | 12,900 | 23,514 | -65% |

| 2 BHK split with roommate | 18,207 | 12,900 | 5,307 | -29% |

| Koramangala 1 BHK | 24,074 | 11,000 | 13,074 | -54% |

| HSR Layout 1 BHK | 24,268 | 10,000 | 14,268 | -59% |

| Whitefield 1 BHK | 26,976 | 9,299 | 17,677 | -66% |

| Electronic City 1 BHK | 23,667 | 3,511 | 20,156 | -85% |

| HelloWorld Cornerhouse HSR (premium) | 24,268 | 35,000 | -10,732 | +44% (more expensive) |

Co-living = per bed. Flat = per unit. Solo occupancy assumed unless noted. 2 BHK split = flat rent divided by 2.

The furnished comparison is the most honest one for new arrivals. Co-living is inherently furnished, all-inclusive, and zero-brokerage. A furnished 1 BHK at Rs 21,989 plus a typical one-month brokerage (another Rs 21,989) makes the first year’s true cost significantly higher than co-living, even before counting deposits.

The one exception: premium co-living at the HelloWorld Cornerhouse tier (Rs 35,000/bed in HSR Layout) is more expensive than renting a 1 BHK flat outright. At that point, you are paying for the brand, the community, and the amenity stack, not for savings.

Co-living vs Flat Market: Full Price Spectrum in Bengaluru (2026)

Section 3: Area-wise breakdown

| Area | Flat avg 1 BHK | Co-living range | Cheapest co-living | vs flat |

|---|---|---|---|---|

| Koramangala | Rs 24,074 | Rs 11,000 to Rs 30,000 | Rs 11,000 (HelloWorld forum) | -54% |

| HSR Layout | Rs 24,268 | Rs 10,000 to Rs 35,000 | Rs 10,000 (HelloWorld tranquil) | -59% |

| Indiranagar | Rs 24,971 | Rs 11,379 to Rs 15,451 | Rs 11,379 (Zolo Aikin) | -54% |

| Whitefield | Rs 26,976 | Rs 9,299 to Rs 13,799 | Rs 9,299 (Stanza Sao Paulo) | -66% |

| Electronic City | Rs 23,667 | Rs 3,358 to Rs 16,299 | Rs 3,358 (Zolo Euphoria) | -86% |

| Manyata / Thanisandra | ~Rs 22,000 | Rs 4,968 to Rs 10,599 | Rs 4,968 (Zolo Marydale) | -77% |

| Bellandur | ~Rs 22,000 | Rs 9,594 to Rs 19,899 | Rs 9,594 (Zolo Zeppelin) | -56% |

Co-living prices are per bed. Flat prices are per unit. Solo occupancy assumed.

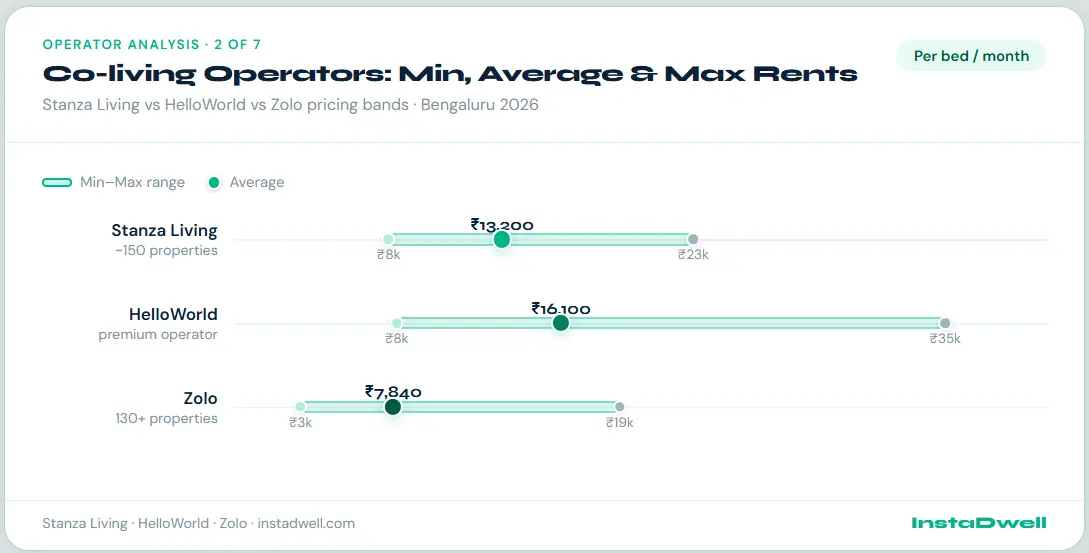

Section 4: The three operators

Zolo: the budget leader with a secret premium shelf

Zolo operates the largest geographic footprint, covering 25+ localities, and its city-wide average of roughly Rs 7,840/bed makes it the clear budget leader. For fresh graduates, first-time migrants, and IT workers on starter salaries, Zolo is often the only viable option.

But the data reveals something most users miss: Zolo quietly runs a shadow premium tier in specific high-demand IT pockets.

- Zolo Triloha, Bellandur: Rs 18,976/bed

- Zolo Sienna, Kasturi Nagar: Rs 16,770/bed

- Zolo Loft, Hoodi: Rs 13,429/bed

These properties are priced at nearly 2.4x Zolo’s own average, competing directly with Stanza’s mid-market range. When a micro-market is close enough to a major tech campus (Manyata Tech Park, RMZ Ecospace, Bagmane), Zolo will push its ceiling. Budget branding does not constrain micro-market pricing.

Stanza Living: the reliable mid-market workhorse

Stanza’s 130+ properties run from Rs 7,599 to Rs 22,599, with most clustering in the Rs 12,000 to Rs 16,000 band. Its geographic spread is the widest of the three: Koramangala, HSR, Mathikere, Manyata Tech Park, Bellandur, Electronic City, Whitefield, the Reva University corridor, and beyond.

Stanza plays a consistent mid-market game in most areas. The notable exception is Bellandur, where Stanza pushes into genuine luxury territory (Brussels House at Rs 19,899, Seattle House at Rs 17,799, Bochum House at Rs 17,399). More on this below.

HelloWorld: the premium operator with suburban ambitions

HelloWorld’s 40+ properties run from Rs 8,000 to Rs 35,000, with a strong concentration in Koramangala and HSR Layout. Its brand positioning is squarely premium: high-design spaces, curated communities, and amenity-forward properties.

The data shows this positioning is now moving outward:

- helloworld arden, Singasandra: Rs 19,999/bed

- helloworld millennium, Nagar: Rs 22,000/bed

These are suburban and peripheral corridors, not established co-living hotspots. HelloWorld is betting that premium demand will follow IT campus expansion into the periphery, pricing ahead of the curve rather than reacting to it.

Head-to-head operator pricing by locality

When placed side-by-side in Bengaluru’s most competitive micro-markets, the brand hierarchies break down entirely based on location. Here is the average monthly rent comparison across the major hubs:

| Locality | Zolo | Stanza Living | HelloWorld |

|---|---|---|---|

| Koramangala | ₹7,200 | ₹15,200 | ₹17,166 |

| HSR Layout | ₹8,400 | ₹18,899 | ₹16,500 |

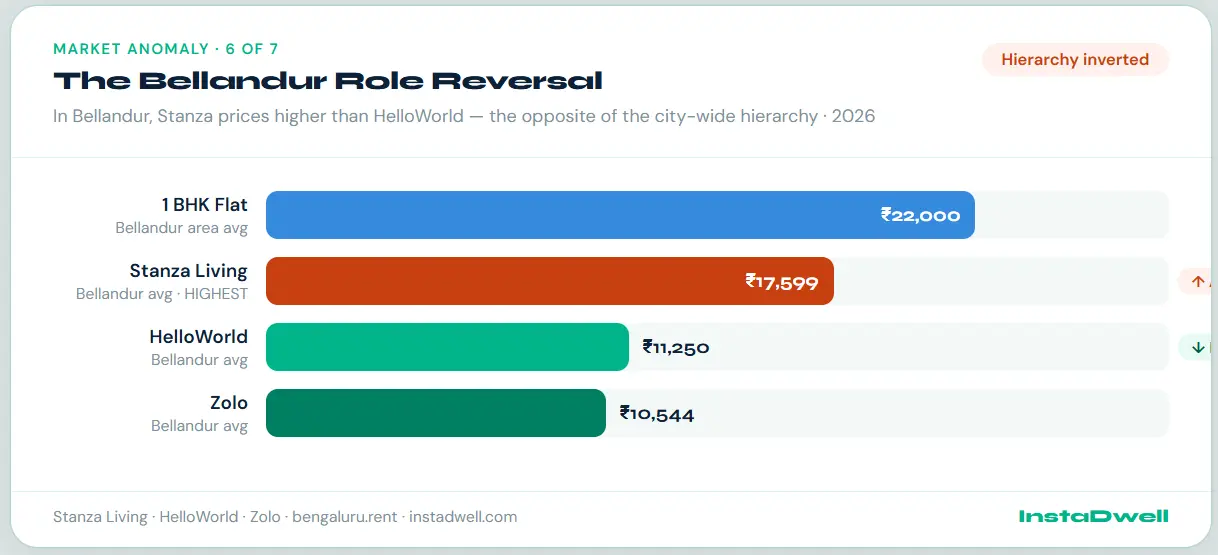

| Bellandur | ₹10,544 | ₹17,599 | ₹11,250 |

| Indiranagar | ₹10,600 | No Data | ₹12,000 |

| Electronic City | ₹5,000 | ₹12,549 | ₹8,000 |

| Marathahalli | ₹4,600 | ₹10,099 | No Data |

Notice how Stanza Living is more expensive than HelloWorld in HSR Layout and significantly more expensive in Bellandur, entirely inverting HelloWorld’s broader brand positioning as the premium option.

Co-living Operators: Min, Average & Max Rents in Bengaluru (2026)

Section 5: Plot twists hidden in the data

Plot twist 1: Zolo’s shadow premium tier

While Zolo is accurately described as the budget leader, the data reveals it operates a shadow premium tier in specific high-demand IT pockets. Rather than sticking to its Rs 7,000 to Rs 8,000 average, it has properties like Zolo Triloha in Bellandur commanding Rs 18,976 and Zolo Sienna in Kasturi Nagar priced at Rs 16,770. This shows that even budget operators will push their ceilings when the micro-market allows for it.

Plot twist 2: Bellandur’s role reversal

Throughout most of Bengaluru, HelloWorld is the luxury option while Stanza plays mid-market. In the tech hub of Bellandur, this dynamic is completely flipped.

Stanza Living in Bellandur (luxury tier):

| Property | Rent |

|---|---|

| Brussels House | Rs 19,899 |

| Seattle House | Rs 17,799 |

| Bochum House | Rs 17,399 |

| Rimini House | Rs 16,999 |

| Shanghai House | Rs 16,899 |

HelloWorld in Bellandur (budget tier):

| Property | Rent |

|---|---|

| helloworld cairo | Rs 11,000 |

| helloworld oswald | Rs 11,500 |

Stanza’s Bellandur average (~Rs 17,500) is nearly 55% higher than HelloWorld’s Bellandur average (~Rs 11,250). This reflects fundamentally different property types, building vintage, and target tenant segments within the same locality.

Implication for renters: In Bellandur specifically, HelloWorld is the budget play, not Stanza. This completely inverts the general market heuristic.

Market Anomaly: The Bellandur Role Reversal (2026)

Plot twist 3: The hyper-budget sub-Rs 4,000 tier

Below Zolo’s standard average lies a dedicated “hyper-budget” tier that rarely gets discussed: a cluster of beds priced well under Rs 4,000/month, located within walking or commuting distance of Bengaluru’s most expensive employment corridors.

| Property | Area | Monthly rent |

|---|---|---|

| Zolo Euphoria | Electronic City Phase 1 | Rs 3,358 |

| Zolo Pepper | Marathahalli | Rs 3,429 |

| Zolo Asmi | Marathahalli | Rs 3,629 |

| Zolo Hoodi Tower | Hoodi | Rs 3,752 |

| Zolo Ginger | Marathahalli | Rs 3,936 |

| Zolo Atlas | Electronic City Phase 2 | Rs 3,511 |

The cheapest Zolo bed in Electronic City costs Rs 3,358/month. The average 1 BHK flat in the same area costs Rs 23,667. That is a gap of over Rs 20,000/month in the same pin code. This sub-Rs 4,000 tier exists because operators can still run profitable density models at these price points in areas where land costs are relatively contained.

Plot twist 4: Premium co-living bleeding into the suburbs

HelloWorld’s price ceiling was once confined to Koramangala, HSR Layout, and Indiranagar. The 2026 data shows premium co-living is now testing suburban and peripheral corridors that previously had no premium rental product at all.

- helloworld arden, Singasandra: Rs 19,999/bed (a low-density IT feeder zone, not a co-living hotspot)

- helloworld millennium, Nagar: Rs 22,000/bed (one of the highest co-living prices outside the core)

At Rs 22,000, this product is priced above the city-wide 1 BHK flat average (Rs 19,064). Premium co-living operators are no longer just competing with flats. They are creating demand in areas where premium rental supply previously did not exist.

Section 6: Who should choose what?

Co-living makes sense if:

- Your budget is under Rs 15,000/month

- You are new to Bengaluru and need a ready-to-move-in solution

- Your stay is 6 to 18 months

- You want zero brokerage and zero deposit hassle

- You are comfortable with shared common areas

- You work near Electronic City, HSR Layout, Koramangala, Manyata, or Whitefield tech hubs

- You value community and networking over privacy

Flat rental makes sense if:

- You are staying 2+ years and want stability

- You have a roommate to split a 2 BHK (per-person cost drops to ~Rs 18,207, competitive with mid-tier co-living)

- You need a dedicated work-from-home room

- You want a gated society or car parking

- Your per-person budget is Rs 15,000+ when split with a roommate

- You prioritise space and privacy over all-inclusive services

The nuanced middle ground

The 2 BHK split scenario is the honest competitor to co-living. Two professionals splitting a 2 BHK at Rs 36,414 pay ~Rs 18,207 each, only Rs 5,307 more than the co-living average, for significantly more space and privacy. The real tipping point is not price; it is how much risk and friction you are willing to absorb to find, negotiate, and set up that flat in the first place.

Section 7: What the market signals for 2026 to 2027

Operators are breaking their own branding rules. Zolo pricing above Rs 18,000 in Bellandur, HelloWorld pricing in Singasandra at Rs 19,999: these are signals that operators are following demand signals rather than maintaining brand lanes. Expect more convergence across tiers over the next 12 to 18 months.

The gated flat premium (15%) is under pressure. As co-living in gated-style properties becomes more common, the justification for paying Rs 2,694 more per month for a gated flat weakens, particularly for solo tenants.

The furnished premium (22%) is co-living’s strongest structural advantage. For tenants who need a furnished place, the co-living product is effectively even cheaper than the headline rent suggests. That 22% furnished premium (Rs 4,007/month) should be added back to any unfurnished flat comparison.

Sub-Rs 4,000 co-living is a policy story, not just a market story. The existence of beds at Rs 3,358 in Electronic City tells you that Bengaluru’s housing market cannot organically serve entry-level migrant workers through the open flat market. The co-living sector, specifically Zolo’s hyper-budget tier, is filling a gap that formal housing policy has not.

Listing Count by Area: Co-living vs Flat Market (2026)

Data sources and methodology

| Source | Coverage | What it covers |

|---|---|---|

| bengaluru.rent | 4,583 pins across Bengaluru | Crowdsourced flat rents: BHK type, gated/not-gated, furnished/unfurnished, area averages |

| Stanza Living via Instadwell | 130+ Bengaluru properties | Co-living property names, locations, starting rents |

| HelloWorld via Instadwell | 40+ Bengaluru properties | Co-living property names, locations, starting rents |

| Zolo via Instadwell | 160+ Bengaluru properties | Co-living property names, locations, starting rents |

Notes:

- Co-living rents quoted are starting/minimum rents for a bed in a shared room unless otherwise specified.

- Flat rents are averages across all pins in each area; ranges vary significantly within each locality.

- All data is point-in-time (2026); rents fluctuate with market conditions.

- Gated society and furnished premiums are city-wide averages, not area-specific.

- The report does not factor in security deposits (typically 2 to 3 months for flats, 1 to 2 months for co-living) or brokerage (typically one month’s rent for flats, nil for co-living operators listed here).

Analysis compiled May 2026.